The sun can wait: Why growth not equal profits?

We support development and engineering efforts for making nascent technologies available, with qualities and efficiency that surpass today’s silicon-based solar technologies performance.Materials research is where we can start, particularly those that could achieve higher conversion ratios to energy or cheaper, and widely available than the rare earth elements used in battery storage.

June 22, 2018. By Moulin

SOLAR POWER

The sun can wait; Why growth not equal profits?

Ricardo G Barcelona, Managing Director of Barcino Advisers

We support development and engineering efforts for making nascent technologies available, with qualities and efficiency that surpass today’s silicon-based solar technologies performance. Materials research is where we can start, particularly those that could achieve higher conversion ratios to energy or cheaper, and widely available than the rare earth elements used in battery storage. For now, the wind, the tide, the rivers and falls, and the earth’s core, could offer better alternative energy supplies than the sun. Use them first when they are available – the sun can wait for its dawn to usher the day of its glory.

Author, Professorial Lecturer, and Adviser. He obtained his PhD in Management, King’s College London, and MBA, IESE Business School. He lectures in leading business schools. He served in senior roles at Royal Dutch Shell, London, United Kingdom, and Den Haag, the Netherlands, and voted top rated equity analyst and adviser, while at SBC Warburg and ABN Amro/Rothschild, London, United Kingdom.

Part of this article is based on selected chapters from the author’s new book – Energy Investments: An adaptive approach to profiting from uncertainties. London: Palgrave Macmillan (www.amazon.co.uk/RGB).

The sun shines brightly. Install solar panels, and we have “free” energy. This narrative, while alluring, is seriously flawed. I am all for clean energy to prevail. However, “exuberant altruism” may prove insufficient to achieve this end. Good economics may offer a more durable route to decarbonize the energy systems. Resource availability – the sun – is one thing. To make the sun an economic and reliable source of energy for humanity to use, the cost should fall farther in converting sunlight into energy. This may require major breakthroughs that could render present silicon-based technologies uncompetitive, or even obsolete. For this reason, rapid costs decline and rapid installation growth resulted in the firms’ parlous financial performance. There are at least three paradoxes at play:

- Drasticcosts decline could result in lower energy prices that reduces cash flows, while facing continual expenditures on upgrades;

- First movers are locked into expensive costs that are stranded when future supplies could cost less; and

- Cash burn rates accelerate with rising installations that exert greater pressure on the firms’ or governments’ finances, with little prospects for closing the gaps.

At the root of these observed phenomena is the learning curve. Costs of photovoltaic solar power (PV), in theory, could fall by 20% for every doubling of installed capacity. While rapid expansion is a cause to celebrate, sharp falls in costs are followed shortly with deep price discounts that wipe out any short-lived advantage. Instead of ushering an era of financial bonanza, declining revenues and constant costs become sure-fire formula for perpetuating losses – and bankruptcies.

Subsidies are resorted to close the revenue gaps, but as energy prices fluctuate, PVs are seen to be paid too little or too much. This creates revenue uncertainties that deter investments. When energy prices are persistently low, more subsidies are needed to keep PV afloat. However, this is the market condition that is least conducive to doling out more subsidies. Consumers quickly realize that they are underwriting expensive investments, where the investors take little risks. Consumers take dual hits: pay more for their energy and get taxed to fund the subsidies.

Late-movers’ advantage: Counter-current thoughts

PV enjoys zero fuel costs but suffers from low conversion rate of sunlight to energy. It is not available when it is most needed – at night. Optimistically, conversion is pegged at 22% with degradation setting in within five years, subject to how good the maintenance is. This implies that to produce similar outputs as coal or gas-fired power generators, where utilization rates are 85% to 87%, PV would need to install more capacity. The equivalent is about four times (1 MW / 0.22 * 0.85 = 3.86 MW). In effect, the comparable capital expenditure at $1,000/kW is $3,860/kW for the equivalent for coal production, or $5,667/kW on a life cycle average of 15% conversion rate. Hydro and geothermal are about $2,000/kW to $2,500/kW, with conversion rates of 85% and 95% respectively.

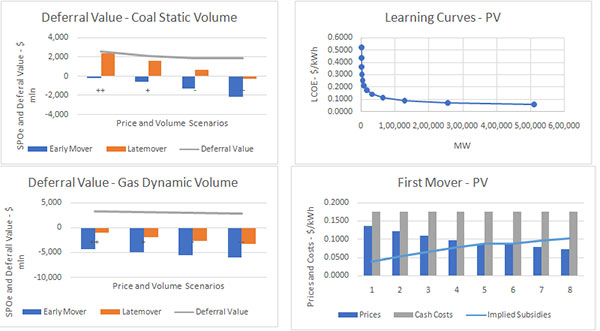

Figure 2: Learning Curves, Deferral Values, and Late-movers’ Benefits

Source : Adapted from Barcelona (2017) , Energy Investments. London: Palgrave Macmillan.

Having established the math, business media’s enthusiasm is curiously premised on logic that underpinned “exuberant altruism”. The argument stands: Learning curves suggest that future PV costs would fall substantially as schematically shown in Figure 2 (Learning Curve – PV). Policy follow this logic by focusing on volume growth. Generous subsidies kickstart the exuberance.As the addiction to subsidies takes hold, its withdrawal inflicts extreme pains to panel producers, as well as investors. Europe’s cuts left the PV industry a trail of bankrupt firms.

How did such benevolent policies fail to deliver?

This brings us to the late-movers’ benefits, a reversal of strategy’s mantra of a first-movers’ win by the bold and the brave, and the fastest.

The first mover (Figure 2 – First Mover – PV) is locked-in with “expensive” supplies. As costs fall, the early movers’ assets are rendered obsolete by technological advances. This could result in one of two scenarios: a) Subsidies increase over time to close the growing gaps; or in its absence, b) losses spike because of under-recovery when payoffs prove insufficient to recover capital expenditures. Under these conditions, managers may decide to invest now or wait until PV costs have fallen farther.

By waiting, investors forego say two or three years of revenues. In a year, there are 8,760 hours (24 h/day x 365 days/year) available to any power generators. Optimistically, at 22% conversion rate, a kW of solar capacity produces 1,927 kWh a year. For every kW of capacity, the revenue loss is about $134 (or $269 for two years, $402 for three years). Deduct the high – low ranges of operating costs from $95 ($0.0495/kWh * 1,927h) to $28 ($0.0146/kWh*1,927h), the annual cash margins are between $39 and $106 (or $78 to $212 for two years, $117 to $318 for three years). In sun-drenched deserts, operating costs may prove higher where water costs more than oil or gas. The scarce resource – water – is essential to clean and maintain the panels in tip top shape to achieve the high conversion rates assumed in PV investments.

PV’s installed costs range from $1,500/kW to $1,000/kW, with some suppliers quoting below $1,000/kW. These costs ranges are consistent with the latest rounds of Saudi Arabia / Softbank offers. Roof top solar panels are stuck at $3,000/kW to $3,500/kW. Since 2014, production and installation efficiency accounted for most of the costs reductions, with more slack left for farther efficiency gains. Conversion rates improved marginally given the silicon’s limitations as energy carrier.

.jpg)

This is a far cry from $4,000/kW to $5,000 kW as recent as 2010. Managers looking at these data would do this quick math: To be indifferent, solar costs should fall less than 5.2% to 21.2% in two years, or from 7.8% to 31.8% over three years. With advocates suggesting a more drastic fall, waiting two or three years could prove more lucrative. On a more realistic note, power prices fell when oil prices fell from $140/bblin 2008 to less than $40/bblin 2010 before rebounding to $70/bbl in 2018. To make PV financially viable, it is racing against the pace it succeeds in reducing costs, and the rate oil prices erodes (or reinforces) its revenues under competitive energy markets.

While coal is presented as the epitome of what is wrong with today’s energy, energy prices under coal-dominated systems tend to be higher, hence friendlier to PV’s economics (Figure 2: Deferral Value – Coal Static Volume). Under very high (++), high (+) or low (-) power price scenarios, the late-movers could achieve positive portfolio values by virtue of the higher energy prices. The early mover, in contrast, could only contribute positively when energy prices are very high (++). Consequently, deferring actions could offer the prospect of lower capital outlay and higher positive payoffs.

Gas’ dominance shift the energy prices lower, given ACCGT’s lower supply costs. This implies a squeeze on Coal and PV’s revenues (Figure 2: Deferral Value – Gas Dynamic Volume). PV’s financial prospects drastically deteriorate under all price scenarios considered. PV could only survive financially with large injections of subsidies or the willingness of altruistic consumers to pay above market prices for their energy. In this case, managers would rather wait for longer. Under highly subsidized regimes, its longevity would depend on how long payments are sustained under increasingly hostile political contexts. As consumers realize that PV investors take little financial risk, while kept afloat at their expense, consumers would coax regulators to cut subsidies.

Reframing niches and strategic moves

PV enthusiasts aspire to replace coal and ACCGTs with “free” energy from the sun. While some markets are getting long term PV supplies at attractive prices, falling energy prices should sound the alarm for the longevity of firms. Under this market, the narratives of “competitive PV” in relation to Coal and ACCGTs, are hard put to co-exist with demands for continued subsidies and tax incentives. The divide is clear: either PV matured to stand on its own, or it remains expensive as to warrant continued subsidies.

The desert or the tropics are fertile grounds to deploy PV. Using auctions to let developers bid for new capacity, Saudi Arabia – Softbank established new records with a bid of less than US$0.02/kWh (TwoCentsPV). The aggressive pricing may secure footholds for new entrants, how they could sustain their financial viability is quite another story. Worse, existing PV suppliers may shake in their boots to see how long their more lucrative price deals would last. What a difference a month makes: From universal acclaim (BigVision), doubts and political infighting are souring the initial enthusiasm from “exuberant altruism”.

Could this be a prelude to recovering good economic sense? Perhaps, or maybe not. The road to perdition is littered with big visions and the carcasses of failed ventures. However, today’s “sharing economy” emerged from the ashes of the dotcom bubble that wiped out fortunes of the brave and the brightestin 2001.

The experience of a smaller scale PV project offer cautionary tale. In the midst of frequent sandstorms, the project produced 315 Wp from 328,320 modules(Sandstorms). While the sun may shine brightly in middle eastern deserts, the sandstorms may simply cancel out any “free energy” when it covers PVs with sand most of the time. In the tropics, hurricanes and dust may do as much damage.

The lessons that are yet to be learned are many. Utilities scale PV is a major user of space and water to keep the panels clean to operate efficiently. In desert conditions, while space is hardly a problem, water is premium commodity that often costs more than oil or gas. In short supply, lack of water may scuttle the best laid plans for massive deployment in sun-drenched middle eastern terrains.

PV’s narratives change for isolated energy markets. Without interconnections, or infrastructures to accept fuel deliveries, communities may have to rely on small hydro, slim-hole geothermal or PVs. Perhaps, this is where the niches for PV could be established more securely. Economics become a conversation around the costs of not having access to energy, rather than the costs to deliver. With this reframing, the economic and social costs of gaining access to energy appear to converge more closely. Thus, the situation of pushing “expensive” PVs to well-connected markets, reverses itself into a pull for bridging energy supplies that PV could well satisfy.

These are possible areas where micro-grids, battery storage, and similar emergent technologies could be tested and deployed. Where they are deployed is a question of matching what are available, and what the communities could affordably absorb.

The subsidies?I would support development and engineering efforts for making nascent technologies available, with qualities and efficiency that surpass today’s silicon-based solar technologies performance. Materials research is where we can start, particularly those that could achieve higher conversion ratios to energy or cheaper, and widely available than the rare earth elements used in battery storage.

For now, the wind, the tide, the rivers and falls, and the earth’s core, could offer better alternative energy supplies than the sun. Use them first when they are available – the sun can wait for its dawn to usher the day of its glory

please contact: contact@energetica-india.net.

Bharath Krishna Rao

CEO & Co-founder

India's EV Future Depends on Localised Manufacturing Says Emobi CEO Bharath Rao

Praveen Kakulte

Founder and CEO

O&M of RE Assets Has Evolved into an Intelligence-Led Function: Praveen Kakulte

Raahul Hari Nair

Founder

The Future Belongs to Energy-Intelligent Enterprises, Says CHI'GRIDS' Founder Raahul Hari Nair

Dibakar Roy

Founder and CEO

Automation, AI and Smart Manufacturing Emerge as Biggest Draw at SNEC 2026: Dibakar Roy

Hiren Pravin Shah

Managing Director and CEO

Renewable Expansion Without Storage will put Increasing Stress on the Grid: Hiren Pravin Shah