Results from India’s Market Survey on Electric Vehicles Expectations

The transportation sector alone accounts for about one-third of the total crude oil consumption and road transportation accounts for more than 80% of this consumption. Therefore the Indian government is focusing on the sector and is keen to partner with the industry for investing in sustainable mobility solutions for the future.

June 26, 2018. By Moulin

ELECTRIC VECHICLES

Results from India’s Market Survey on Electric Vehicles Expectations

Energetica India

The transportation sector alone accounts for about one-third of the total crude oil consumption and road transportation accounts for more than 80% of this consumption. Therefore the Indian government is focusing on the sector and is keen to partner with the industry for investing in sustainable mobility solutions for the future.

Abbrevations

- HEV= Hybrid Electric Vehicle

- xEV= Full range of Electric Vehicles

- 2W= Two Wheeler

- 3W= Three Wheeler

- 4W= Four Wheeler

- BEV= Battery Electric Vehicle

- PHEV= Plug-in-Hybrid Electric Vehicle

In a study jointly conducted by the Department of Heavy Industry (DHI) and the industry has come up with in-depth understanding of the issues involved in adaptation of EVs in India, challenges ahead and also gives an estimate of possible latest demand of xEVs in the country. The study involved extensive field level consumer surveys based on direct interaction.

Three Possible Scenarios Of Demand Projection For India

In case of India, three most likely future scenarios of vehicle demand projection have been considered for the purpose of analysis andoutcome development. These are:

- Scenario 1 – Status- quo:

This scenario assumes that there is no change in the current state of fuel mix and the penetration patterns of the respective vehicle segments remain similar to the current pattern i.e. ʹ high ICEpenetration and `marginal CNG penetration.

- Scenario 2 – The High Gas and High HEV

Here significant government focus on CNG and xEV through investments and incentives has been considered. This scenario underlines a strong xEV focus to substitute IC engine technology. Here a substantial CNG penetration of about 30-35% andsignificant Hybrid penetration of 10-15% has been assumed by 2020 for vehicles other than 2W. The BEV penetration has been taken to be low, reaching about 2% in 2020. However, in view of the ease of deployment of BEV two wheelers, 15% penetration in sales by 2020 is taken in this scenario.

- Scenario 3 - High Gas, High HEV and High BEV

This is one step ahead of the high gas/HEV scenario and takes into account a strong focus on BEVs in addition to CNG and HEV. Here the BEV penetration is assumed to increase to 5% in 2020 (by sales) across most vehicle segments, while capturing 15% of 2- wheeler market.

In addition, estimates of the likely impact of these penetration levels on future liquid fuel consumption have been made for both the High Gas/High HEV and High Gas/High HEV/High BEV scenarios in order to estimate the possible savings by 2020 and also the likely cost – benefit analysis for the initiative.

Important Findings of the Government – Industry Study

In-depth study comprising of an extensive ground level consumer survey based on direct interviews and administered questionnaires was carried out. The study included several rounds of focused group discussions covering all major cities and demographic groups and interactions with key stakeholders were also conducted. The Joint Government – Industry study provided an understanding of the consumer preferences, and the likely effective divers for adoption of hybrid and electric vehicles in India. This study forms the basis for arriving at the latent xEV demand projections for India.

The field survey for four and two wheeler vehicle segments involved more than 1800 consumers across 16 cities, while that for buses and three wheelers entailed170 interviews of bus fleet owners across 11 cities and 1600 consumers respectively to understand their preferences. The interviews with bus fleet owners were extensive and 75%-80% of bus population in tier 2, 3 and 4 cities and 40%-50% bus population in tier 1 cities were covered.

The Focus Group Discussions (FGD)

The Focus Group Discussions with potential consumers providedseveral significant insights, such as

(i) Currently there is a limited understanding of xEV technologies amongst the consumers.

(ii) Consumers are willing to pay a premium of 10-20% for HEVs justified by their lower operating costs; however the premium should be recoverable in 2-3 years.

(iii) Highest preference has been expressed for HEVs, followed by PHEVs and BEVs – due to lack of charging requirement,higher range, lack of battery replacement, availability of an IC engine as a backup to the electric engine etc.

(iv) Consumers appeared to be more receptive to PHEVs and BEVs, if there is an TCO model acceptable range and if the necessary charging infrastructure is available.

(v) Charging aspects was citedas being important and most respondentspreferred public charging infrastructure and lower charging time. The charging time anxiety was higher for two wheelers and three wheeler owners.

(vi )Environmental benefits of xEVs did not appear to be an important buying criterion for consumers.

Industry Feedback

The insights gained fromthe OEMs, research institutesand component suppliers indicates that

(i) the lowdemand for xEVs in Indianmarket is due to high price, low performance, lack ofinfrastructure and lowawareness.

(ii) HEVs seem to be preferred due to higher range and no chargingissues as compared to PHEVs and BEVs.

(iii) Amongst the various vehiclesegments, the easiest uptake of xEVs will be for buses, two wheelers followed byfour wheelers and three wheelers.

Total Cost of Ownership (TCO) Model

Demand Projectionsbased on Consumer survey,FGDs, TCO analysis: Based onextensive consumer surveys,focus group discussions,interactions with differentstakeholders, including OEMs and TotalCost of Ownership (TCO) analysis model, Industry feedback the study has made estimations for thepossible latent demand projections forxEVs by 2020. These are summarizedbelow.

Four Wheelers:Consumer research has revealed that overall there is a high latent demand for xEVcars (4W) and that 25-30% ofsurveyed consumers wouldprefer a xEV to traditional ICEfour wheelers (4W) providedprice & performance expectations aresuitably met. Amongst the xEV fourwheelers, the higher preference is for HEV (~14-15%) followed by PHEV (~9-10%F) carsand least for BEV cars (~5%). The mainbarriers inhibiting adoption of 4W BEVs are poor pick up, low top speed and issues relating to battery replacement.

Projections based on thetotal cost of ownership (TCO) analysis for 4Ws indicate that with suitable incentives being provided; the four wheeler xEVs will have significant latent demand by 2020.The likely potential demand for 4W will be in the range of ~ 1.6-1.7 million units by 2020. In this projection, it is assumed that the scale effects will come into play in2020 and lead to 10% reduction inacquisition price. Within 4W xEVs, mildhybrid and full hybrid EVs can have alatent demand of ~20% by 2020 due to their lower acquisition and operatingcosts. The 4W HEVs are likely to have a latent demand of ~4% by 2020 and 4WBEVs can have a latent demand varyingfrom 2.5% -5% based on cost. It is alsoclear that on its own, the xEV potential for4Ws in India will not be reached by 2020unless consumer expectations are met.The study indicates that demand sideincentives would be critical. In addition,technology and infrastructureimprovements would also be required forrealizing the latent demand for 4W xEVs.

Two Wheelers:Consumer researchindicates that although electrictwo wheelers have much higheracceptance, yet poor pick up, lowtop speed and batteryreplacement issues continue tobe the main barriers to higher adoption ofxEV 2W. The demand projections basedon TCO analysis indicate significant latentdemand for BEV two wheelers which isprojected to rise from 2% at present to~16% by 2020. This corresponds to ~5Million units by 2020 constituting 16% ofthe total future projected demand of 32million two wheelers. Depending upon thefuture petrol prices, it is estimated thatthe latent demand could be in the rangeof 20% for BEV scooters and 15% for BEVbikes by 2020 to as high as 21% in a moreaggressive scenario. Further, consumerresearch also indicates that there is ahigher preference for battery operated2Ws (~55-60%).

Buses:Higher preference has been expressed for hybrid buses byconsumers compared to PHEVand BEV buses. The key barriers for early adoption of xEV buses include pick up, battery replacement and charging time. In order to harness theexisting latent market potential leading to increased xEV adoption, incentivizing both consumers and manufacturers would berequired. The demand side incentives can push up demand thus enabling the OEMs to achieve scale thereby reducing theproduction costs and make the busesmore affordable. It would therefore beVs preferable to front load the incentives to drive early adoption and then phase out the incentives. By 2020, the likelypotential demand for xEV buses will be in the range of 2300 - 2700 units.

LCVs:Consumer surveyindicates that the key barrierswhich may inhibit the adoption of xEV LCVs include poor pick up,low top speed and high batteryreplacement costs. In case the demandincentives and other enabling conditions are met, it is expected that by 2020 HEV and BEV LCVs may achieve a penetration level of 8% and 4% respectively. In volume terms, this translates to 81,000 units and 35,000 units of HEV and BEV LCVsrespectively.

Three Wheelers:Pick up and top speedemerged as the top two key barriers inhibiting adoption of threewheeler xEV technologies along with battery replacement cost. It isexpected that with demand incentives, latent demand for 3W BEVscan be more than 2% by 2020.

The impact of technology and economies of scale on demand: It is expected that improvements intechnology and global scale effect willbring down lithium ion battery costs byabout 5-7% YoY in future, thereby translating to price level of $325 - $430/kWh by 2020. However, these prices would still remain higher than equivalent price expectation of the Indian consumer ($ 210-275/ kWh) leading to a higher acquisition cost than consumer expectation. This aspect has been taken into account while arriving at the likely xEV demand projections for India by 2020.

The projections for possible xEV latent demand in India along with the Global projections for 2020 are summarized in Table 1&2.

.jpg)

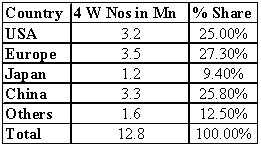

Table 1: India and Global xEV demand Projections for 2020 (nos in millions

Table2: Projected Global Share of 4W xEV

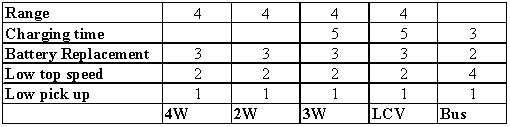

The summary of the vehicle segment wise barriers for adoption of xEVs, as indicated in preceding paras, is summarized in Table 3. It must be remembered that this feedback is in context of the comparisons that consumers made in the performance of traditional IC engine vehicles with xEVs. In addition, it must also be appreciated that the current consumer understanding of xEVs is alsolimited. However, these barriers relating to performance will need to be overcome by ensuring that xEVs that are introduced in the market meet certain specified minimum requirements.

Table3: Vehicle segment-wise matrix of key barriers to xEV adoption

The otherimportant findings ofthe study in regard to

(i) Key consumerpurchase criterion forxEV.

(ii) Sensitivity analysis across four key parameters ofprice, running costs, recharging time and range.

(iii) City wise variations in xEVdemand.

(iv)Consumer preference for incentive type.

(v) Possible niche usage areas for xEVs are summarized as follows.

Key Consumer Purchase Criteria

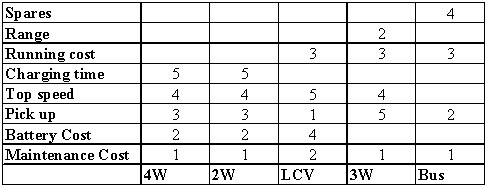

Consumers have expressed maintenance cost, battery cost, pickup, top speed and charging time as major factors considered while buying xEV two wheelers and four wheelers. In case ofLCVs top factors considered while buying xEV LCVs are pick up, Key maintenance costs and running costs. The top factors indicated by consumers while buying three wheeler xEVs were maintenance costs, range and running costs. Maintenance costs, pick up, running costs and availability ofspares are important to 60% consumers and therefore emerge as the key factors considered by consumers while buyingxEV buses. A summary of the key consumer purchase criteria fordifferent vehicle segments is captured in Table 4.

Table4: Vehicle segment-wise matrix of key consumer purchase criteria

Sensitvity analysis across key parameters

Sensitivity analysisacross four key parameters ofprice, running cost, rechargetime and range was conductedas a part of the conjoint analysison consumer feedback receivedfrom various cities. This gives agood understanding on theextent of the impact that anychanges to these parametersare likely to have on theconsumer preference.Therefore, this helps inidentifying the parameters ofmaximum impact in each of thevehicle segments. This analysis reveals thefollowing:

In case of 4W, theconsumers are highly sensitive to priceand running cost of HEV cars; with greaterpreference for lower acquisition costs.This implies that cash incentives and fuel efficiency can serve as effective levers to is across key parametersincrease the adoption of 4W HEVs.Therefore, OEMs should also focus onimproving fuel efficiency for HEVs, andspreading awareness of the same.Similarly, in case of 4W PHEVs and BEVslowering of acquisition cost can beeffective in stimulating demand. The faceto face consumer interviews validated theefficacy of acquisition cost basedincentives and battery subsidies for 4WxEVs.

Similar to the 4W segment in case of 2W also, consumers are mostsensitive to acquisition price. In addition, consumers have also shown sensitivity to recharging time. This indicates thatincentives on BEV 2W is likely to beeffective in boosting demand. Theadoption of fast/quick chargers is alsolikely to help generate demand.

In case of LCVs, in addition to acquisition price, consumers haveshown sensitivity to running costs. As such cash incentive on acquisition costs is likely to be effective. Further, lower chargingtime is also important and will lead to an increase in latent demand in case ofPHEVs.

Like most other segments, in bus segments also consumers haveexpressed sensitivity around acquisitionprice. Hence, cash incentives would beeffective and will be essential to generate demand. Moderate sensitivity was also

Acquisition price remainsthe major concern in the three wheelersegment as well. Running cost, chargingtime and range are also areas of majorconcern to consumers. These concernscan be mitigated through roll-out of fastand rapidcharging terminals and publiccharging infrastructure.

The summary of theoutcome of the sensitivity analysis for the various vehicle segments across the four parameters is given in Table 5. Thisclearly indicates that gains through higher fuel efficiency and demand incentives will be the key levers for higher xEV off take.

Table5: Sensitivity Analysis Matrix for different vehicle segments

City-wise Variations

Consumer feedbackfrom 16-18 cities reveals thatthere are significant variationsacross cities. An analysis of theresponses received across variouscities reveals that in case of xEVs,four wheelers and LCVs havehigher uptake in Tier 1 and 2cities as compared to the Tier 3 and 4cities. In case of LCVs, Tier 1 and Tier 3 cities have shown a higher preference for HEV than BEV/PHEV. In case of 3W, higher preference has been expressed in tier 2 and tier 4 cities. As far as the battery operated two wheelers is concerned, there is a high latent demand for thesevehicles specifically in tier 2 cities followed by tier 1 cities. The respondents in tier 1 and 2 cities have also cited highestpreference for low maintenance cost and high mileage. The tier wise breakup shows that in the bus segment, HEVs are mostpreferred and that HEVs have the highest preference in tier 2 and 4 cities; whilePHEV and BEV buses are most preferred in tier 4 cities. State Road TransportCorporations in cities like Bangalore andDelhi have evinced interest in xEV buses.

Consumer preference for type of incentive

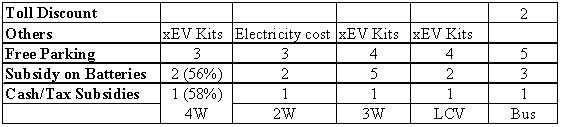

In case of 4W,consumer interviews indicate thatcash/tax subsidies would be thepreferred (58% respondents)mode of demand incentive foradoption of 4W xEVs. The cash ortax incentive can be given directlyto an OEM or to the consumereither directly or routed throughthe OEM. Subsidy on batteriesemerged as the second mostfavored route (56% respondents).However, battery subsidies maynot be required in the near termas the advent of Li ʹ ion batteriesin cars delays the replacement of batteriesto 7-10 years after purchase. Lowerpreference has been indicated for otherperipheral benefits such as dedicated tolllanes, toll discounts etc. In case of twowheelers, low/no tax and low cost ofbatteries have been cited as the mostimportant motivators for adoption of xEV2 W by the consumers. In case of threewheelers, the preferred form of incentivesindicated was low/no tax, retro fit kitavailability and free/reduced cost ofpermits. For LCVs, consumers indicatedno/low tax and availability of low costbatteries as the preferred incentivemodes. In case of buses, surveys indicatethat cash support, toll discounts and lowcost batteries are the most preferredConsumer preference for typ incentive. Further, as in the case of 4Walso, it is also expected that with the use of lithium ion batteries in buses, battery replacement may be required in 5-7 years. As such the replacement of batteries is not expected to be a barrier in future,therefore, upfront acquisition costs onlyneed to be supported. The consumer preference for type of incentive issummarized in Table 6.

Table6: Vehicle segment-wse matrix of consumer preference for Incentives

However, it must also be remembered that the incentive delivery mechanism that is adopted should be simple andeffective that allows the incentive to reach the intended beneficiaries quickly andefficiently. As already indicated, theexisting/earlier schemes leave a lot ofscope for improvement in this regard. Possible niche area of usage/applications for xEVs: In case of thevarious vehicle segments, the xEV variants lend themselves to niche area applications/usage. Some of these include:

- The premium bus segment(low floor A/C) can be a target for xEVsbuses, as price points are high (Rs. 1-1.3Crore for xEVs compared to Rs. 60-70Lakhs for ICE bus). However, prices for xEV high floor bus would be very high ascompared to a high floor ICE bus (~Rs. 70- 80 Lakhs compared to Rs. 25-30 Lakhs for ICE). Hence, xEV adoption in low floor buses (like DTC buses) may be moreviable.

- Small buses used for lastmile connectivity for metro stations willalso be highly amenable for xEVs due to their usage pattern.

- xEV LCVs can be used inniche applications such as airport pick-ups, transportation within factory premises etc. Rapid charging stations may need to beestablished to increase adoption of such vehicles.

- Low speed 3W BEVs can beused in pockets with high traffic, small campus and small towns.

Source: “National Electric Mobility Mission Plan 2020.” Department of Heavy Industry Ministry of Heavy Industries and Public Enterprises Government of India.

please contact: contact@energetica-india.net.

Bharath Krishna Rao

CEO & Co-founder

India's EV Future Depends on Localised Manufacturing Says Emobi CEO Bharath Rao

Praveen Kakulte

Founder and CEO

O&M of RE Assets Has Evolved into an Intelligence-Led Function: Praveen Kakulte

Raahul Hari Nair

Founder

The Future Belongs to Energy-Intelligent Enterprises, Says CHI'GRIDS' Founder Raahul Hari Nair

Dibakar Roy

Founder and CEO

Automation, AI and Smart Manufacturing Emerge as Biggest Draw at SNEC 2026: Dibakar Roy

Hiren Pravin Shah

Managing Director and CEO

Renewable Expansion Without Storage will put Increasing Stress on the Grid: Hiren Pravin Shah